As banks navigate the operational complexities of 2026, the global financial landscape is defined by a clear directive: modernize or risk obsolescence. For years, syndicated and corporate lending have been the anchor of manual processes and legacy systems. Today, however, we are witnessing a paradigm shift where cutting-edge technology platforms are no longer just “nice-to-have”; they are the foundational infrastructure for survival.

But there is a vital lesson that many banks are learning the hard way: technology alone is not a silver bullet. The true differentiator in this era of rapid change isn’t just the solution in which you invest, but the expertise with which you implement it. In my view, the “implementation gap,” the space between a platform’s theoretical capability and its practical operational reality, is where the future of banking will be won or lost.

The Modernization Imperative: Beyond the Software

The traditional model of managing multi-lender structures, bespoke covenants, and cross-border transactions through siloed data is evolving. With rising regulatory expectations and the rapid expansion of private credit, banks and financial institutions now require a level of agility that legacy systems are increasingly being outpaced by, creating an opportunity for more advanced, integrated solutions.

Forward-thinking banks and financial institutions are recognizing that a successful digital transition requires more than just a capital investment in a new platform. It requires a deep understanding of the complex business and credit processes that the technology is designed to serve. This is where the role of specialized implementation partners becomes critical. FINEXCORE has emerged to bridge this gap, focusing on aligning sophisticated lending systems with the complex operational realities of modern banking.

4 Pillars of a Successful Digital Lending Transition

Large Banks: The Titans of Complexity

Beyond specific solutions, any successful implementation depends on a strategic framework. Based on the trends we’re observing in 2026, here are the four essential pillars that determine whether a technology deployment delivers real business value.

1. Process Re-Engineering Over Simple Configuration

Too often, banks attempt to “pave the cow path” by simply digitizing their existing, inefficient workflows. A successful implementation starts with meticulously mapping current-state processes and identifying automation opportunities before a single line of code is configured. The goal should be to design a future-state operating model that leverages the platform’s full potential for straight-through processing.

2. Seamless Integration Across the Ecosystem

In 2026, corporate lending systems must communicate flawlessly with core banking, risk management, and treasury tools. This requires a robust integration architecture often driven by modern APIs and middleware to ensure that data flows accurately and in real-time across the entire network.

3. Specialized Capabilities for Emerging Frontiers

As global finance becomes more diverse, technology must adapt to specialized needs. One of the most significant shifts seen is the demand for Sharia-compliant lending solutions. Banks and financial Institutions in the Gulf and Southeast Asia face the unique challenge of running structures like Murabaha or Ijara on platforms often designed for conventional interest-based lending. Success here depends on partners who understand both the technical configuration and the stringent requirements of Sharia governance.

4. Bridging the Knowledge Gap Through Targeted Training

The most sophisticated platform in the world is ineffective if your team doesn’t know how to use it. Generic training programs often fail because they don’t address the specific business requirements product mix or workflows of the banks. Specialized, role-specific training for loan administrators, relationship managers, and IT teams is essential to minimize operational errors and ensure long-term sustainability.

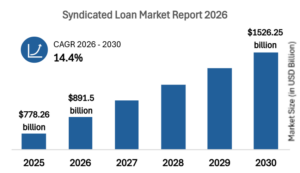

$891B global syndicated loan market size in 2026

Looking Ahead: The Future of Implementation

The trend for the upcoming decade is clear: we will see increased automation, tighter integration with corporate lending systems, and a greater emphasis on real-time data access for all syndicate participants.

For banking and financial institutions, the challenge is to move beyond isolated point implementations toward end-to-end transformation. Whether you are consolidating a legacy technology stack or expanding into new markets like sustainable finance, the focus must remain on the quality of delivery.

In a market defined by rapid digital acceleration, the role of the “implementation partner” has evolved from a technical vendor into a strategic ally. Firms that combine technical depth with genuine practitioner expertise, a model championed by organizations like FINEXCORE, will be the ones that help banks translate digital potential into measurable business outcomes: centralized operations, reduced costs, and the ability to scale without a proportional increase in headcount.

The digital evolution of lending is here. The question is no longer if you will transform, but how effectively you will execute that transformation.

You cannot copy content of this page