And what it tells us about the future of digital banking.

Let me start with a simple question.

Would you hand your passport to a stranger on the street just because it was convenient?

Of course not.

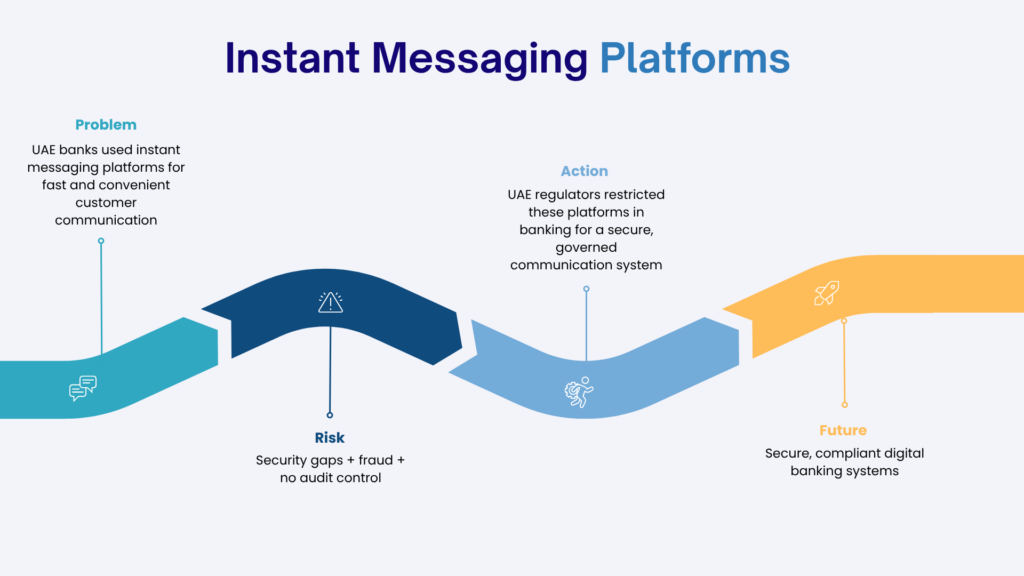

Yet for years, banks around the world have relied on instant messaging platforms like WhatsApp for customer communication and document exchange.

That’s now changing. And the UAE just made it official.

So What Exactly Happened?

Regulators in the UAE have prohibited banks from delivering services and collecting information through instant messaging apps like WhatsApp.

On the surface, it sounds like a small policy tweak.

It isn’t.

This is one of the clearest signals yet that the global banking industry is entering a new chapter, one where the rules of digital communication are being fundamentally rewritten.

And every bank in the world should be paying attention.

Why Did Banks Start Using WhatsApp In The First Place?

Honestly? Because it was easy.

When banks were under pressure to go digital fast, WhatsApp was already everywhere. Customers used it daily. Employees were comfortable with it. Asking someone to photograph their ID and send it over a chat window felt modern and frictionless.

So it stuck.

But here’s the problem nobody wanted to talk about out loud: easy and appropriate are two very different things. Especially in banking.

Here’s The Real Problem With WhatsApp In Banking

WhatsApp has evolved significantly over the years, including the introduction of WhatsApp Business to support business communication at scale.

But even with these advancements, instant messaging platforms were not purpose-built for the complex governance, regulatory oversight, and enterprise-grade compliance requirements that financial institutions operate under.

When banks use these platforms to deliver services and collect sensitive information, they often encounter structural limitations around auditability, control, supervision, and data governance.

Here’s what instant messaging apps like WhatsApp simply cannot provide for banks:

- A proper audit trail: Who sent what? When? To whom? Good luck proving it.

- Document security: Customer files end up in personal employee inboxes, completely outside the bank’s controlled environment.

- Fraud protection: Scammers can easily create fake accounts that look exactly like your bank and ask customers to send their documents. Customers have no way to know the difference.

- Compliance monitoring: There’s no reliable way to track, supervise, or govern these conversations at scale.

- Data governance: When a regulator asks where customer data is stored and how it’s protected, “a decentralized messaging platform” is not an acceptable answer.

These aren’t small technical issues. They are serious structural vulnerabilities that put customers and banks at risk every single day.

Why Are Regulators Acting Now?

Because the threat landscape has changed dramatically.

Financial fraud is more sophisticated than ever. Cybercriminals don’t always try to hack bank systems directly anymore. Instead, they go after the weakest link, and an unverified WhatsApp message asking for your ID documents is one of the weakest links imaginable.

Regulators have looked at this picture and made a clear decision: the risk is no longer acceptable.

But there’s something bigger happening here, too.

Regulators aren’t just asking banks if they’ve gone digital anymore. They’re asking how they’ve gone digital.

Is it secure? Is it transparent? Can you prove accountability at every step? Can you defend every customer interaction in a regulatory review?

If the answer involves WhatsApp, an unmanaged instant messaging platform, that’s a problem.

This Is Bigger Than One App

Here’s what I want you to take away from this.

The UAE’s decision isn’t really about WhatsApp. WhatsApp is just the most visible symptom of a much deeper issue: banks trying to do enterprise-grade work with consumer-grade tools.

And while this regulation starts in the UAE, the same pressure is building everywhere.

In Europe, data protection regulations are getting stricter. In North America, regulators are zeroing in on operational resilience. Across Asia-Pacific, digital banking frameworks are being overhauled with security at the centre.

The direction of travel is clear. Every bank, in every market, will eventually face the same question:

Is your communication infrastructure actually built for the regulated environment you operate in?

From Digital Convenience to Digital Trust

It helps to think about this as two distinct chapters in digital banking’s story.

Chapter One was all about speed and convenience. Get online. Launch the app. Make banking faster. The banks that won were the ones that digitized quickest.

Chapter Two, the one we’re stepping into right now, is about something even more important.

Trust.

Today’s customers have lived through data breaches, identity theft, and a wave of financial scams that have made them deeply cautious about who they share their information with.

They don’t just want a bank that’s digital. They want a bank that makes them feel genuinely safe.

And here’s the insight that the smartest banks are already acting on: security isn’t the enemy of good customer experience. It is the customer experience.

What Does Good Look Like?

The good news is that the alternative to WhatsApp isn’t complexity or inconvenience.

The best banks are building integrated digital ecosystems where:

- Every customer interaction is secure by design

- Every document is tracked, governed, and retrievable

- Compliance happens automatically, not as an afterthought

- Customers can interact digitally without ever feeling exposed

Frictionless on the outside. Bulletproof on the inside.

That’s the standard. And it’s entirely achievable.

This is exactly where enterprise communication platforms are becoming critical.

Solutions like FINEXCORE CommBridge are designed specifically for regulated financial environments, enabling banks to securely manage customer communications, document exchange, approvals, and workflows within a fully governed ecosystem.

Instead of scattered conversations across instant messaging apps, platforms like CommBridge centralize interactions with built-in audit trails, access controls, compliance monitoring, and secure document handling, giving both regulators and customers far greater confidence.

That’s the standard. And it’s entirely achievable.

The Bottom Line

The UAE’s WhatsApp ban is a wake-up call.

Not just for banks in the Gulf. For every bank and financial institution that has been quietly relying on informal, ungoverned communication channels and hoping it wouldn’t become a problem.

What was once considered convenient is now being recognized as a growing risk.

But more importantly, and this is the key point, fixing it is also a genuine opportunity.

Banks that move quickly to adopt secure, compliant, enterprise-grade communication infrastructure won’t just satisfy regulators. They will earn deeper customer trust, reduce operational risk, and build a more resilient business for the long term.

The era of WhatsApp banking is ending.

What comes next is smarter, safer, and arguably long overdue.

At FINEXCORE, we help banks and financial institutions build secure, intelligent, and compliance-ready digital ecosystems for modern banking.

With solutions like CommBridge, banks can move beyond fragmented instant communication tools and create a secure engagement layer built specifically for the realities of regulated financial services.

Because in the future of banking, trust won’t just be built through products.

It will be built through every interaction.

You cannot copy content of this page